Your comprehensive analysis will include:

Retirement savings projections

Retirement savings projections- An overview of potential retirement income by account type

- Estimates of how long savings may last under different scenarios

- General resources to help inform retirement planning

About This Calculator

To estimate how much you may need to save for retirement, we begin by calculating how much you're expected to spend over the course of your retirement. This includes estimating the income you'll need based on your lifestyle preferences, then factoring in how many years you may spend in retirement. We assume a lifespan of 95 by default, though you can adjust it after your calculation is complete. Once we have a clearer view of your total retirement needs, we use our models to evaluate your existing and future resources. This includes estimating retirement income from Social Security and the impact of current retirement plans, pensions, and other accounts.

Assumptions

Lifespan: We assume you will live to 95. We stop the analysis there, regardless of your spouse's age.

Retirement accounts: We automatically distribute your future savings optimally among different retirement accounts. We assume that the IRS contribution limits for your retirement accounts increase with inflation.

Social Security: We estimate your Social Security income using your stated annual income and assuming you have worked and paid Social Security taxes for 35 years prior to retirement. Our estimate is sensitive to penalties for early retirement and credits for delaying claiming Social Security benefits.

Return on savings: We assume the percentage return on your savings differs by whether you're pre- or post-retirement and by account type, with a distinction between investment accounts and savings accounts. This assumption does not account for market volatility or investment losses and assumes positive growth over time. All investing involves risk, including the possible loss of principal.

SmartAsset.com is not intended to provide legal advice, tax advice, accounting advice or financial advice (Other than referring users to third party advisers registered or chartered as fiduciaries ("Adviser(s)") with a regulatory body in the United States). Articles, opinions, and tools are for general information only and are not intended to provide specific advice or recommendations for any individual. The retirement calculator is meant to demonstrate different potential scenarios to consider, and is not intended to provide definitive answers to anyone's financial situation. We always suggest that you consult your accountant, tax, legal or financial advisor concerning your individual situation.

This is not an offer to buy or sell any security or interest. All investing involves risk, including loss of principal. Working with an adviser may come with potential downsides such as payment of fees (which will reduce returns). Past performance is not a guarantee of future results. There are no guarantees that working with an adviser will yield positive returns. The existence of a fiduciary duty does not prevent the rise of potential conflicts of interest.

Planning for Retirement

Edited by

Edited by  Reviewed by

Reviewed by Your retirement readiness comes down to one comparison: how much income you’re projected to have versus how much you’ll need. Our calculator estimates both over your retirement timeline, combining your savings, Social Security and other assets on one side, and your expected spending on the other.

If those totals align, you may be on track. If there’s a gap, it indicates that your current inputs may not support your target lifestyle. From there, you can adjust key assumptions, such as your savings rate, retirement age or expected income, to see how different scenarios affect your results.

Do you need professional help planning for retirement? Speak with a financial advisor today.

How to Use Our Retirement Calculator

The retirement calculator gathers information in three main steps: your personal details, your savings and your retirement goals. Each step feeds into that comparison, estimating how much income you may have versus how much you say you’ll need.

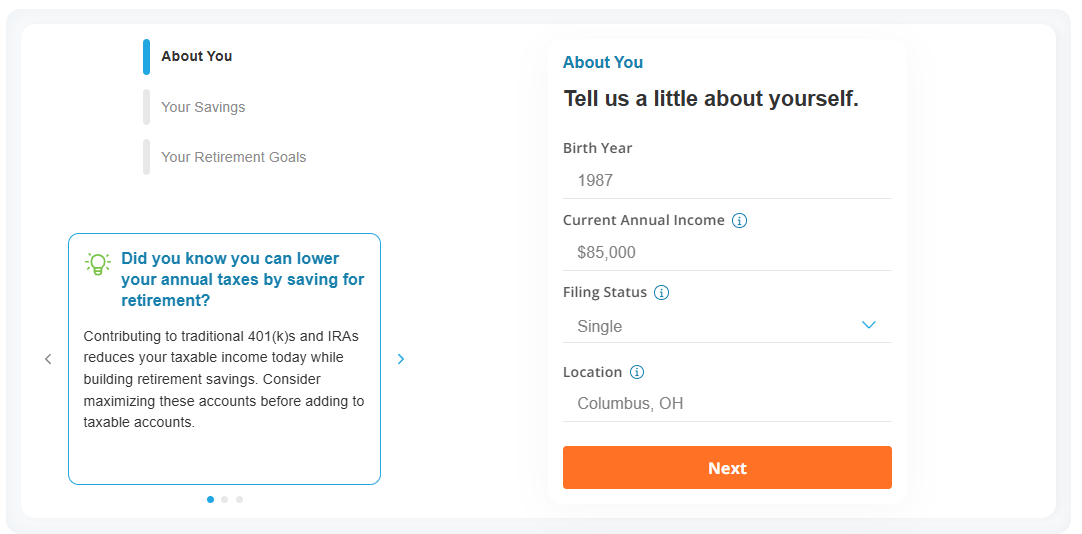

1. Enter Your Personal Details

This first step establishes the foundation for your analysis. Your age, income, tax filing status and location help determine your working timeline and shape key assumptions, such as how long your savings have to grow and how taxes may affect your income over time.

These details provide the context the calculator uses to interpret your savings and retirement goals more accurately.

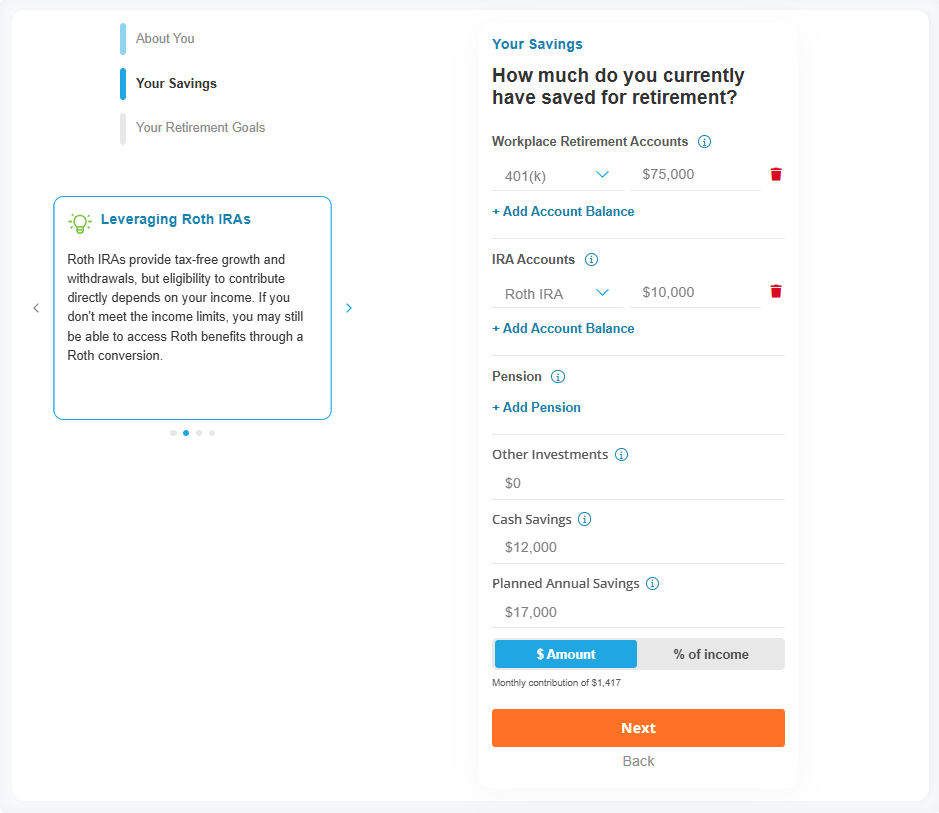

2. Add Your Retirement Savings

This section focuses on the assets you’ve already accumulated and what you plan to contribute going forward. The calculator combines your existing balances, ongoing savings and expected investment growth to project how your assets may grow before retirement and how they may be drawn down afterward.

By including different account types, such as workplace plans, IRAs and other investments, the model can estimate a more complete picture of your potential retirement income, rather than relying on a single source.

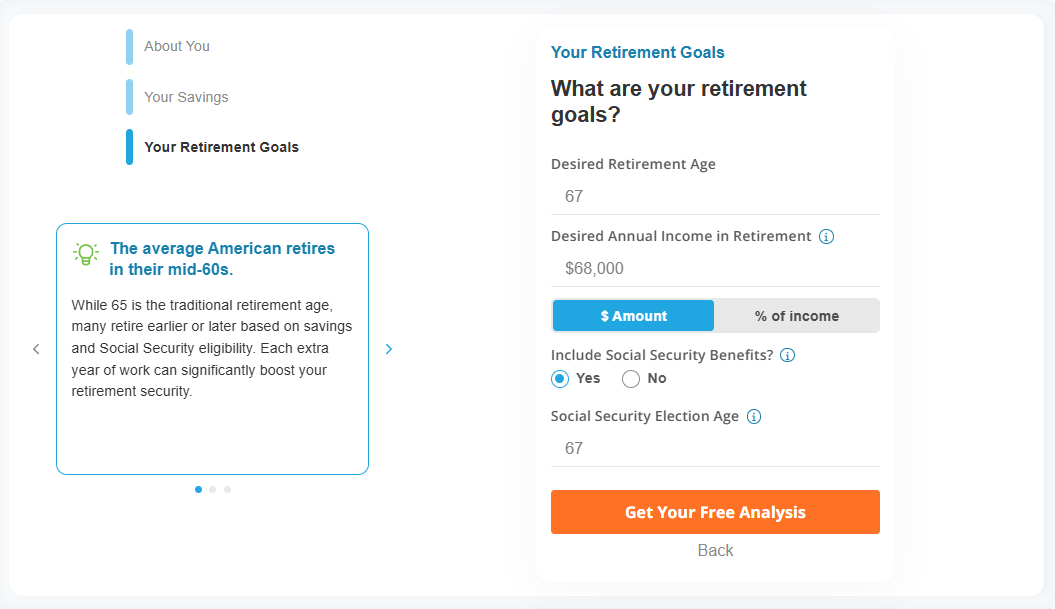

3. Set Your Retirement Goals

Here, you define your expectations for retirement. Your desired retirement age sets the length of your timeline, while your income goal establishes the spending level the calculator is trying to support. You can enter this as a dollar amount or as a percentage of your current income.

These inputs form the “how much you’ll need” side of the equation, which is then compared against your projected income. Including Social Security adds another layer, helping estimate how much of your income may come from guaranteed sources versus personal savings.

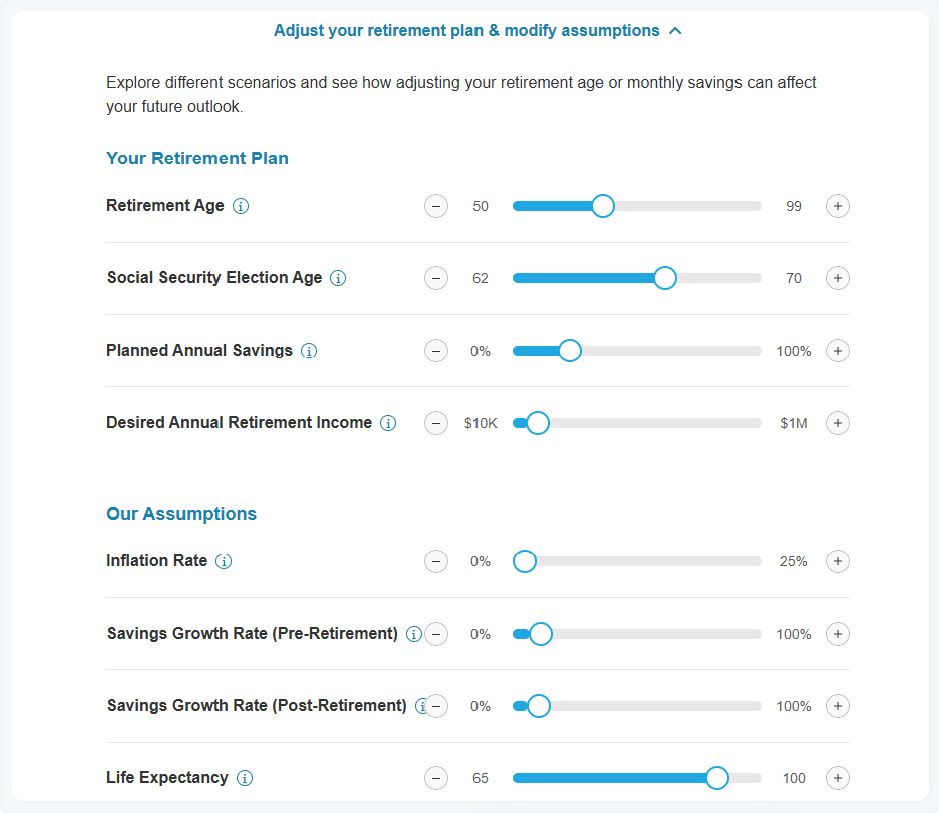

4. Review and Adjust Your Results

After entering your information, the calculator compares your projected income to your expected needs to determine whether you are on track or off track.

You can view your results as a total amount over retirement or as estimated annual income. From there, you can adjust assumptions, such as savings, retirement age, Social Security election age, inflation or investment returns, to see how different scenarios may affect your analysis.

What Drives Your Retirement Projection

Several assumptions influence your results, and adjusting them can change whether you appear on track or off track.

Savings and Contributions

How much you have in savings and how consistently you contribute both have a direct impact on your projected income. Increasing contributions over time can improve outcomes through compounding.

Retirement Age

Your planned retirement age affects both how long your savings have to grow, how long they need to last and how much your Social Security benefits will be. Retiring later allows for more time to save and fewer years of withdrawals.

Investment Returns

Your expected rate of return influences how your savings grow before retirement and how they are drawn down afterward. Small changes in return assumptions can lead to different projections over long time horizons.

Other Income Sources

Social Security, pensions and other income streams can reduce how much you need to rely on personal savings and can play a meaningful role in your overall projection. While there isn’t a specific input for annuities, you can plug your annuity income into the pension field to estimate how it could impact your outlook.

How to Improve an “Off Track” Projection

If your results show that you are off track, there are several ways to adjust your plan:

- Increase your savings rate: Contributing more each month can help grow your balance over time

- Delay retirement: Working longer allows for additional savings and reduces the number of years your assets need to support you

- Adjust your spending expectations: Lowering your target retirement income can reduce the total amount needed

- Revisit your assumptions: Modifying inputs such as investment returns or inflation can change your projected outcome

- Review your investment strategy: Aligning your portfolio with your time horizon and risk tolerance may improve long-term growth potential

How Inflation Affects Your Results

Inflation plays a key role in shaping your retirement outlook by influencing both how your savings grow and how much income you may need over time. As prices rise, the same level of spending requires more dollars, which can increase your total retirement needs.

The calculator accounts for inflation by adjusting investment returns and long-term projections so that your results are shown in today’s dollars, making it easier to compare income and spending on a consistent basis.

You can adjust the inflation assumption to see how different scenarios may affect your plan. Higher inflation may increase the amount you need to support your lifestyle, while lower inflation may reduce that pressure.

Rules of Thumb for Retirement Planning

While every situation is different, general guidelines can provide a starting point:

- 10% to 15% rule: Saving 10% to 15% of your income is often cited as a baseline, but many households may need to target closer to 15% to 20%, especially if they start saving later or expect a longer retirement. If your calculator results show you are off track, gradually increasing your contribution rate is one of the most direct ways to improve your outlook.

- 4% rule: This approach suggests withdrawing 4% of your savings in the first year of retirement and adjusting that amount for inflation each year after. More recent updates suggest that a slightly higher withdrawal rate (4.7%) may be sustainable.

- Income replacement guideline (70% to 80%): Many people aim to replace 70% to 80% of their pre-retirement income. This can help you estimate your target spending, which feeds directly into the “how much you’ll need” side of your results. Your actual target may be higher or lower depending on factors like housing costs, healthcare and lifestyle choices.

- Savings milestones by age: Another way to track progress is by comparing your savings to your income at different ages. A common guideline suggests saving 1x your salary by age 30, 3x by age 40 and 6x by 50. These benchmarks can help you evaluate whether your current savings pace aligns with your long-term goals.

Retirement Benchmarks and Adjustments

Benchmarks can offer context for how your savings compare to others, though they do not account for differences in income, spending, retirement age or goals.

According to the Vanguard’s “How America Saves 2025” report, the average account balance within defined contribution plans was $271,000 for people between ages 55 and 64, while the median account balance was nearly $96,000. 1 The gap between the average and median suggests that higher-balance savers pull the average upward, while the typical saver has far less set aside.

That median is also a reminder of how undersaved many Americans are as they approach retirement. For someone in their late 50s or early 60s, a balance below $100,000 may not generate enough annual income to support a multi-decade retirement, especially when healthcare costs, inflation and longevity risk are factored in.

| Age Group | Average Account Balance | Median Account Balance |

|---|---|---|

| Under 25 | $6,899 | $1,948 |

| 25-34 | $42,640 | $16,255 |

| 35-44 | $103,552 | $39,958 |

| 45-54 | $188,643 | $67,796 |

| 55-64 | $271,320 | $95,642 |

| 65 and older | $299,442 | $95,425 |

Ways to Strengthen Your Retirement Plan

There are several strategies that can help build or improve your retirement savings over time:

- Contribute consistently to a 401(k), especially if your employer offers a match

- Open and fund an IRA to supplement workplace savings

- Increase contributions as your income grows

- Automate savings to maintain consistency

- Consider tax strategies such as Roth conversions, depending on your situation

- Diversify your portfolio to balance growth and risk

- Delay Social Security to increase your monthly benefit

- Explore options like SEP IRAs or Solo 401(k)s if you are self-employed

Finally, you may also want to talk to a financial advisor if you are close to retirement and want to fine-tune your plan, need help reviewing your investment or withdrawal strategy or want to confirm that your assets are aligned with your long-term goals. SmartAsset’s free matching tool can pair you with advisors who serve your area.

Frequently Asked Questions (FAQs)

How accurate are the investment return assumptions?

The calculator uses long-term average returns based on an 80/20 stock-bond portfolio before retirement and a 60/40 portfolio during retirement (both adjusted for inflation). Actual market performance can vary from year to year, so it can be helpful to test more conservative and more optimistic scenarios to see how different outcomes may affect your plan.

Why does the calculator show a total amount instead of just a retirement balance?

The calculator focuses on the total amount your savings can generate over your retirement timeline, not just what you accumulate by the time you retire. This reflects how retirement works in practice, where your savings are gradually converted into income rather than used all at once.

How should I think about Social Security in my plan?

Social Security can reduce how much you need to withdraw from savings. Claiming at 62 typically lowers your benefit by about 25% to 30%, while delaying past full retirement age increases it by about 8% per year up to age 70. Adjusting your claiming age can change your overall projection.

Article Sources

All articles are reviewed and updated by SmartAsset’s fact-checkers for accuracy. Visit our Editorial Policy for more details on our overall journalistic standards.

- How America Saves 2025. Vanguard, June 2025, https://corporate.vanguard.com/content/dam/corp/research/pdf/how_america_saves_report_2025.pdf.