Overview of Property Taxes

Property taxes in America are collected by local governments and are usually based on the value of the underlying property. The money collected is generally used to pay for community safety, schools, infrastructure and other public projects. Use SmartAsset's tool to better understand the average cost of property taxes in your state and county.

| Enter Your Location Dismiss | Assessed Home Value Dismiss |

| Average County Tax Rate 0.0% | Property Taxes $0 (Annual) |

| of Assessed Home Value | |

| of Assessed Home Value | |

| National | of Assessed Home Value |

- About This Answer

To calculate the exact amount of property tax you will owe requires your property's assessed value and the property tax rates based on your property's address. Please note that we can only estimate your property tax based on median property taxes in your area. There are typically multiple rates in a given area, because your state, county, local schools and emergency responders each receive funding partly through these taxes. In our calculator, we take your home value and multiply that by your county's effective property tax rate. This is equal to the median property tax paid as a percentage of the median home value in your county.

What Are Property Taxes?

When you buy a home, you'll need to factor in property taxes as an ongoing cost. It’s an expense that doesn’t go away over time and generally increases as your home appreciates in value.

What you pay isn’t regulated by the federal government. Instead, it’s based on state and county tax levies. Therefore, your property tax liability depends on where you live and the value of your property.

In some areas of the country, your annual property tax bill may be less than one month’s mortgage payment, but in others, it can get quite a bit pricier. With property taxes being so variable and location-dependent, you’ll want to take them into account when you’re deciding on where to live.

A financial advisor can help you understand how homeownership fits into a larger financial plan. Speak with an advisor today.

What Do Property Taxes Pay For?

Property taxes help fund many public services in your local area. A large part of this money goes to public schools, helping to pay for teachers, school buildings, supplies and other education costs. In many communities, schools are the biggest share of the local property tax budget.

These taxes also support services like police, fire departments and emergency medical services. They help pay for the people, buildings and equipment needed to keep communities safe. Local roads, snow removal and public transportation may also be funded through property taxes.

In addition, property taxes help pay for libraries, parks and city or county government offices. These funds keep basic services running and help maintain public spaces that everyone uses. The amount collected and how it's spent can vary depending on where you live.

Key Terms You Should Know When Calculating Property Taxes

There are a few key terms that you should know when estimating how much money you could owe to your local government. Here are 11 terms to help you get a clearer understanding:

- Market value: This is the estimated amount that your home could sell for under normal conditions. It is often based on recent sales of similar properties and is the starting point for calculating your property tax.

- Assessment rate or ratio: This is the percentage of your property’s market value that is subject to taxation. The rate can vary by state and property type.

- Assessed value: This is the taxable value of your property and your tax bill is based on this figure. To calculate it, multiply the market value by the assessment rate.

- Millage rate: The millage rate shows how much tax you pay for every $1,000 of a property’s assessed value. One mill equals $1 in tax per $1,000 of assessed value. For example, a millage rate of 20 mills means you pay $20 for every $1,000 of assessed value.

- Mill levy: This is the total tax rate applied to your property, based on the combined needs of your city, county, school district and other local entities. The mill levy is a product of the millage rate.

- Taxable value: This is your assessed value minus any applicable exemptions. It’s the final number used to calculate your tax before credits are applied.

- Exemptions: These are reductions in taxable value for certain groups, such as seniors, veterans, people with disabilities or low-income homeowners. They help lower your total tax bill.

- Tax credits: Unlike exemptions, which reduce taxable value, credits reduce the final amount of tax owed. Not all areas offer credits, so availability varies by location.

- Excess levies: These are additional taxes approved by voters for specific purposes, such as school funding or public safety, and are added to your base tax rate.

- Property improvements: Adding features like a new room, garage or finished basement can increase your property’s market and assessed values, which may raise your tax bill.

- Property type: How your property is used (residential, commercial or agricultural) affects how it’s assessed and taxed. Some types qualify for lower rates or specific exemptions.

How Property Taxes Are Calculated

Property taxes can vary widely depending on where you live, but the basic steps to calculate them are similar in most places. Here's a general breakdown with eight steps to help you better understand what you owe and why:

- Find your home’s market value: Check your most recent property assessment or use recent sales of similar homes in your area to estimate your home’s market value.

- Look up your local assessment ratio: Contact your county assessor’s office or visit their website to find the percentage of market value that is taxed in your area. This is your assessment ratio.

- Calculate your assessed value: Multiply your market value by the assessment ratio. As an example, if the assessed value of your home is $200,000, but the market value is $250,000, then the assessment ratio is 80% (200,000/250,000).

- Check for any exemptions: See if you qualify for property tax exemptions (e.g., for seniors, veterans, or people with disabilities). Subtract any exemption amounts from your assessed value to get your taxable value.

- Find your local millage rate: Millage rates are set by your city, county, school district and other taxing authorities. Millage rates are expressed in tenths of a penny, meaning one mill is $0.001.

- Calculate your base property tax: Multiply your taxable value by the total mill rate. For example, on a $300,000 home, a millage rate of $0.003 will equal $900 in taxes owed ($0.003 x $300,000 assessed value = $900).

- Apply any tax credits: Check if your area offers property tax credits. If you qualify, subtract the credit amount from your calculated tax to find your final bill.

- Find out your payment method and schedule: Contact your mortgage lender or county tax office to confirm how and when your property taxes are paid, whether that be monthly through escrow or directly to the county on a set schedule.

How you pay your property taxes varies from place to place. Some people pay extra each month to their mortgage lender. The lender keeps that money in escrow and then pays the government on behalf of the homeowner. Other people pay their property tax bill directly to the county government on a monthly, quarterly, semi-annual or annual basis. Your payment schedule will depend on how your county collects taxes.

Property Tax Examples Using Our Calculator

Here are three examples using data from our property tax calculator to show how property taxes vary by state:

Example 1: Illinois

Illinois has the highest effective property tax rate in the U.S. at 1.92%. That means the median annual property tax bill in Illinois is 1.92% of the median home value. Let's assume you own a home worth $350,000 in Illinois City, which is located in Rock Island County. According to our calculator, your effective property tax rate is 2.25%, giving you the following calculation for your annual property taxes:

$350,000 × 0.0225 = $7,875

Example 2: California

On the other hand, California’s state effective property tax rate is lower at 0.71%. So say you purchase a $500,000 home in San Bernardino County, where the effective rate is 0.67%. That would leave you with the calculation below for your annual property taxes:

$500,000 × 0.0067 = $3,350

Example 3: Texas

Lastly, Texas has another high effective property tax rate of 1.31%. If you bought a $270,000 home in El Paso, your effective property tax rate would be 1.71%. Here's how that would break down:

$270,000 × 0.0171 = $4,617

What Property Tax Exemptions Are Available?

Property tax exemptions can reduce the taxable value of your home if you meet certain rules. Here's a breakdown of five common property tax exemptions that you could benefit from:

- Homestead: This exemption lowers the taxable value of a home that is used as the owner's main residence. It can also give some protection to surviving spouses. The amount and rules depend on the state, and it doesn’t apply to vacation homes or rentals.

- Persons with disabilities: Homeowners with certain disabilities may qualify for a reduction in property taxes on their primary home. Local governments or school districts usually offer these, and proof of disability is often required.

- Senior citizens: Many states or towns offer tax breaks to older adults who meet age and sometimes income requirements. These usually apply to a main residence and may lower the home’s assessed value or freeze taxes at a certain rate.

- Veterans: Veterans, especially those with service-connected disabilities, may get a tax break from their state or local government. The amount can vary based on the level of disability, and some programs also extend to surviving spouses.

- Energy efficiency or renewable energy exemption: Some states or local governments give property tax breaks to homeowners who add energy-saving features like solar panels or geothermal systems. These upgrades can increase your home’s value and the exemption may help you save money on property taxes with them.

Other less common exemptions can include:

- Widow/widower exemption: Available in some areas to surviving spouses who meet certain conditions.

- Agricultural exemption: Applies to land used for farming, ranching or similar purposes.

- Low-income exemption: In some places, homeowners with limited income may qualify for reduced property taxes, even if they don’t meet other conditions like age or disability.

It’s worth spending some time researching whether you qualify for any applicable exemptions in your area. If you do, you can save thousands over the years.

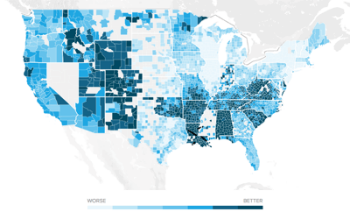

Property Taxes By State

Overall, homeowners in New Jersey pay the highest property taxes, where the median property tax bill is $9,358. The state’s effective rate is 1.89%, meaning the typical homeowner in the Garden State pays 1.89% of their home value in property taxes each year.

Homeowners in West Virginia have the lowest median property taxes in the nation at just $881 per year. The effective property tax rate in the Mountain State is just 0.52%, thanks to a median home value of $170,800.

Meanwhile, Hawaii has the lowest effective property tax rate in the nation (0.27%) but the highest median home value ($875,900). Despite its reputation as a costly place to live, Hawaii has generous homeowner exemptions for primary residents that lower taxable values considerably. The tax break generally helps those who live in Hawaii full-time, rather than those who own a second home there.

Also of note are Colorado and Oregon’s property tax laws, which voters put in place to limit large taxable value increases. Many states don’t have caps on how much property taxes can change annually, but those two are examples of state governments that put laws in place because of taxpayer concern.

Here's a breakdown of the data for all 50 states, according to Census Bureau data:

Frequently Asked Questions About Property Taxes

How often are property taxes assessed?

Property taxes are typically assessed once per year, though the schedule varies by state and county. Some jurisdictions reassess property values annually, while others do so every two, three or even five years. Even if assessments are less frequent, tax bills can still change annually due to adjustments in tax rates or local levies.

Can property taxes increase even if my home value stays the same?

Yes. Property taxes can rise even if your home’s assessed value does not change. Increases can result from higher millage rates, new voter-approved levies or reduced exemptions. Conversely, taxes may decrease if rates fall or additional relief programs are applied.

What happens if I don’t pay my property taxes?

If property taxes go unpaid, the local government can impose penalties and interest. Over time, this may lead to a tax lien being placed on the property or, in extreme cases, a tax foreclosure. Timelines and enforcement procedures vary by jurisdiction.

Are property taxes included in my mortgage payment?

Property taxes are frequently paid through escrow arrangements. When escrow is in place, the lender collects estimated tax amounts as part of the monthly mortgage payment and pays the taxes on the homeowner’s behalf. Without escrow, property owners must pay their tax bills directly to the appropriate local government.