Edited by

Edited by  Edited by

Edited by  Reviewed by

Reviewed by

Converting an IRA to a Roth IRA after age 60 can offer tax-free withdrawals in retirement. Plus, withdrawals from a Roth IRA at age 60 aren’t subject to early distribution penalties or required minimum distributions (RMDs), both of which can increase your tax liability in retirement. However, the process does involve paying taxes on the converted amount upfront, meaning you could face a hefty income tax bill, depending on how much you plan to convert.

Do you have questions about retirement planning and Roth conversions? Speak with a financial advisor today.

How Does a Roth Conversion Work?

The difference between a Roth IRA and other types of IRAs is that a Roth account is funded with after-tax dollars. That means you pay taxes on the funds before contributing them to a Roth account, and you can’t deduct contributions from your taxable income. On the plus side, the money in a Roth IRA grows tax-free, and you can withdraw funds after you retire without paying taxes.

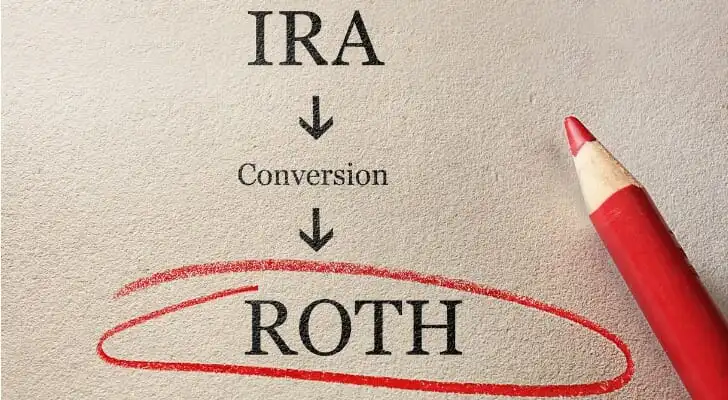

If you have funds in pre-tax IRA accounts, such as a traditional IRA, SEP IRA or Simple IRA, you have the option of converting them to a Roth IRA. When you complete a Roth IRA conversion, you have to pay taxes on that money at your current rate. This can result in a big tax bill for the year when you do the conversion. The amount of the conversion is treated as regular income, which can bump you into a higher tax bracket.

Circumventing Roth IRA Income Limits

A Roth IRA conversion after age 60 can be worthwhile for a couple of reasons. First, it can get around the income caps that limit Roth contributions for those with higher incomes. A person’s eligibility to contribute directly to a Roth IRA depends on their modified adjusted gross income (MAGI), with higher-earning taxpayers losing the ability to contribute to a Roth IRA once their MAGI hits a certain threshold.

For 2025, single filers and heads of household can contribute the full amount ($7,000) if their MAGI is under $150,000, with contributions gradually phasing out up to $165,000. Married couples filing jointly qualify for full contributions if they have a MAGI below $236,000, with the phase-out occurring between $236,000 and $246,000. Meanwhile, married individuals filing separately experience a phase-out within the narrow range of $0 to $10,000.

However, there are no limits on conversions. A taxpayer with a pre-tax IRA can convert any amount of funds in a year to a Roth IRA.

Avoiding RMDs

Another compelling reason for a Roth conversion is that Roth IRAs are exempt from required minimum distributions (RMDs). These mandatory withdrawals from retirement accounts begin at age 73 (75 for people born in 1960 or later) and can create a tax burden on affluent retirees. But Roth owners don’t have to make RMDs for as long as they live, which can make Roth IRAs particularly useful for leaving inheritances.

Plan your retirement withdrawals more effectively using our RMD calculator.

When weighing whether it’s worth doing a conversion to get this benefit, it’s helpful to know how much your RMDs could end up being. You can calculate this by dividing the balance of your IRA as of the prior Dec. 31 by your applicable life expectancy factor, which is published by the IRS. If your RMD is sizable enough to push you into a higher tax bracket, for instance, then a Roth conversion may make sense to do.

Another factor to consider when it comes to Roth IRA conversions is where you plan to retire. If you anticipate relocating post-retirement to a state with high income taxes, a conversion likely makes more sense than if you are retiring to a state with low or no state income tax.

Benefits of Roth Conversions After Age 60

Roth IRAs are popular with younger savers who anticipate being in higher tax brackets later in their working lives. However, they can also be useful for taxpayers over age 60. One reason is that taxpayers in their 60s may be earning less than they did in their peak years, so the income tax bite of a Roth IRA conversion is smaller.

For those with substantial retirement assets and who anticipate receiving pension benefits in addition to Social Security, the RMDs from a traditional IRA can also put them in a higher tax bracket post-retirement. Converting to a Roth IRA now can reduce the post-retirement tax burden, though at the cost of paying some taxes today.

Drawbacks of Roth Conversions After Age 60

The biggest drawback of a Roth conversion is the upfront tax bill on the amount converted. Another consideration is the five-year rule: Roth IRAs must be open for at least five years before earnings can be withdrawn tax-free. Withdrawals of your original contributions are always tax-free, and after age 59½, they’re not subject to the 10% early withdrawal penalty.

However, if you convert funds and withdraw them within five years the earnings portion could be subject to income tax.

Roth IRA conversions aren’t recommended for all savers. For instance, many retirees will have lower incomes than when they were working. For them, it’s likely better to use a traditional IRA and pay taxes when withdrawing funds. Similarly, Roth IRA conversions may not make much sense if a taxpayer intends to leave assets in a traditional IRA to a charity.

Finally, it’s important to note that the process of converting a pre-tax IRA to a Roth IRA can’t be undone. A taxpayer who is not certain whether post-retirement income taxes will be lower than they are today might want to think twice about a conversion.

Bottom Line

For taxpayers who anticipate a higher tax rate post-retirement, converting a traditional IRA to a Roth IRA after age 60 can help to lower their total tax burden over time. Roth IRA conversions allow earnings to grow tax-free and avoid the need to make required withdrawals that increase post-retirement tax costs. Roth IRA conversions come at the cost of having to pay taxes on converted funds now rather than later, however. Also, funds converted after age 60 have to be left in the account for five years before they can be withdrawn tax-free.

Tips on Retirement

- Deciding whether or not to convert traditional IRA assets to a Roth IRA calls for careful evaluation of your financial and tax situation. That’s where a financial advisor can be invaluable. Finding a financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with vetted financial advisors who serve your area, and you can have a free introductory call with your advisor matches to decide which one you feel is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

- Use our free retirement calculator to get an estimate of how you’re progressing toward your retirement goals.

Photo credit: ©iStock.com/designer491, ©iStock.com/zimmytws, ©iStock.com/designer49